National Debt 101 (circa 2025)

I used AI to explain it to me like I'm 5...

Opening disclosure: I used my questions, my initial research and details, but took it to “uber-clippy” to turn my questions into answers. What follows is AI generated, read by me for clarity or as much accuracy as I can provide.

It all started with me wanting to know what this actually “means.”

What National Debt Actually Is

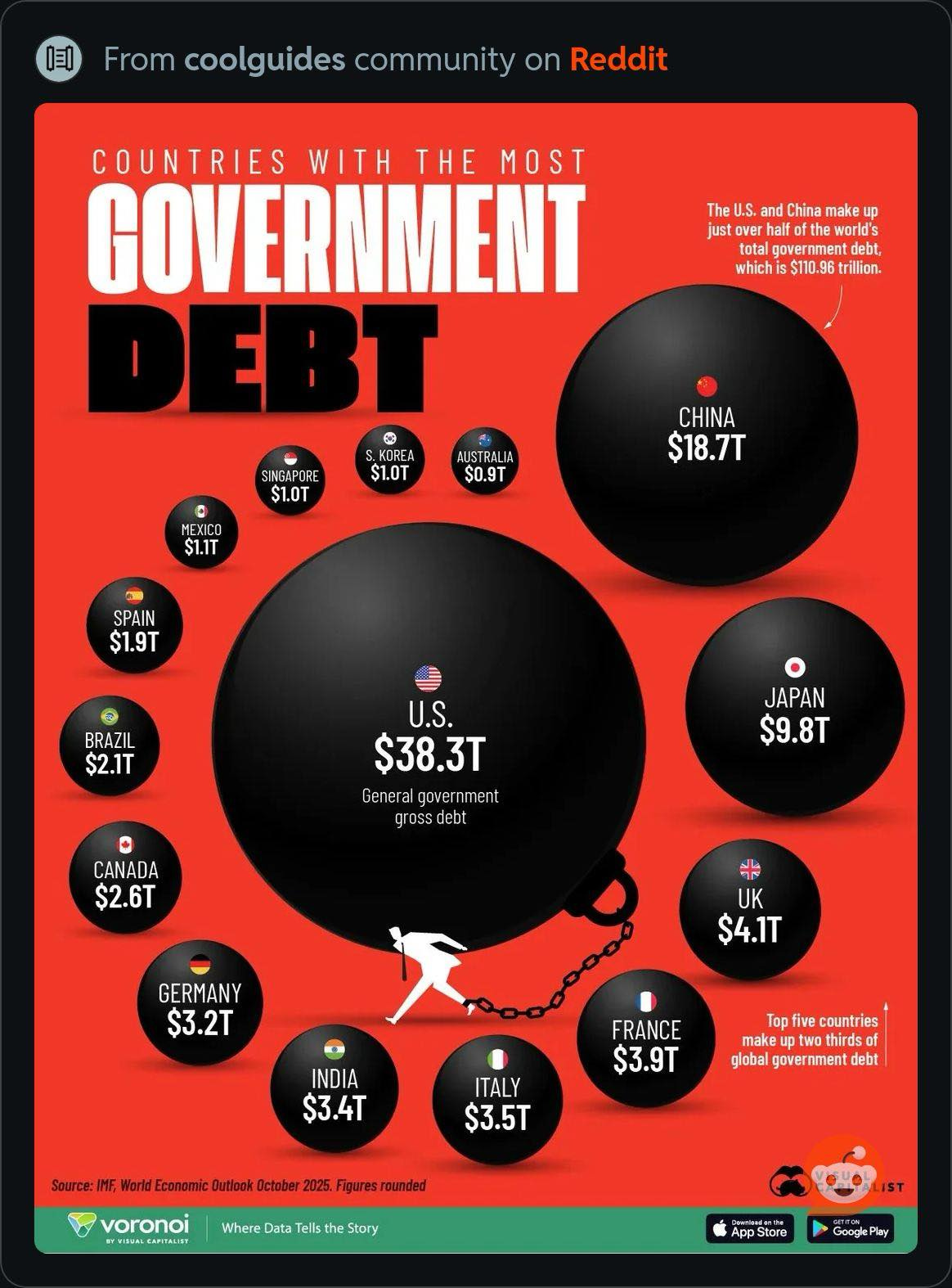

It’s basically government bonds. When the government spends more than it takes in through taxes, it borrows money by selling Treasury bonds (IOUs). People, companies, other countries, and even the U.S. government itself buy these bonds. The $38 trillion is the total of all those IOUs the government has promised to pay back.

The Current Situation (The “Oh Crap” Metrics)

From the chart pack and recent data:

Debt-to-GDP ratio: 122% - This means our total debt is bigger than our entire economy’s annual output. That’s higher than the post-WWII peak.

Interest payments are exploding - The government now spends more on interest than on children’s programs, and interest spending will exceed defense spending by 2027 Committee for a Responsible Federal Budget.

We’re spending about $881 billion per year just on interest - that’s money that does NOTHING except pay the cost of past borrowing.

Why High Debt Is Dangerous (The Real Risks)

Think of it in layers, from “definitely happening” to “potential catastrophe”:

Layer 1: The Slow Squeeze (Already Happening)

High government borrowing puts upward pressure on interest rates throughout the economy, and every dollar the government borrows reduces private investment by about 33 cents (Committee for a Responsible Federal Budget.) This is called “crowding out.”

Here’s what that means practically:

Entrepreneurs pay more to borrow money for new businesses

Companies invest less in innovation and equipment

Over time, this results in lower GDP (1.1% smaller by 2035, 5.6% smaller by 2075), millions fewer jobs, and wages that are 5.3% lower than they would be otherwise (Peterson Foundation)

Your mental model: Imagine the economy as a pie. The government is taking bigger and bigger slices to pay interest on old debt, leaving less pie for everyone else to invest in productive things that actually grow the economy.

Layer 2: Loss of Fiscal Flexibility (The “Rainy Day Fund” Problem)

As one analysis put it: “We are guilty of spending our rainy-day fund in sunny weather” (Fortune.) When the next crisis hits (pandemic, war, financial collapse), we won’t have the borrowing capacity to respond effectively. The more debt accumulates, the less “fiscal space” we have to borrow when we actually need it. (Committee for a Responsible Federal Budget)

Layer 3: National Security & Global Position

The chart pack shows that a huge chunk of discretionary spending goes to defense, veterans, international affairs. But as one former Chairman of the Joint Chiefs said, “The most significant threat to our national security is our debt” (Peter G. Peterson Foundation) - because money spent on interest is money NOT available for defense, cybersecurity, or other security needs.

Plus, about 30% of U.S. debt is owned by foreign investors. The more dependent we are on foreign creditors, the less leverage we have internationally.

Layer 4: The Crisis Scenarios (Low Probability, Catastrophic Impact)

This is where it gets scary. A fiscal crisis would involve a sudden, large, sustained drop in demand for Treasury securities that triggers a sharp spike in interest rates, probably accompanied by a steep fall in the dollar and equity markets, potentially causing a global financial crisis Brookings.

What could trigger this?

Investors lose confidence in the government’s ability to pay, demanding much higher interest rates to hold U.S. debt Committee for a Responsible Federal Budget

Political dysfunction (like debt ceiling fights) makes investors think the U.S. might actually default

The “boiling frog” effect - where the crisis moves in slow motion until suddenly the system breaks Fortune

If this happens, you’d see:

Massive spike in interest rates on everything (mortgages, car loans, business loans)

Inflation potentially spiraling

Dollar losing value

Forced austerity - harsh spending cuts and tax increases all at once

Potential global financial meltdown (since Treasuries are the bedrock of the world financial system)

Why Can’t We Just Keep Borrowing?

The U.S. has unique advantages - the dollar is the world’s reserve currency, Treasury bonds are seen as the safest asset on earth. But economists warn that solutions from the past aren’t available today: we don’t have the favorable conditions of the post-WWII era (very low interest rates plus fast growth), nor the “peace dividend” of the 1990s that allowed defense cuts Fortune.

The most likely outcome isn’t a sudden crisis, but rather a slow and steady erosion of capital and national wealth that impairs living standards for future generations Brookings. We’re essentially borrowing from our kids to fund current consumption.

The Bottom Line

The danger isn’t necessarily that the government will “run out of money” tomorrow (it won’t - it can always print more or keep borrowing). The danger is:

Guaranteed slow decline: Less investment, slower growth, lower wages, reduced quality of life

Lost flexibility: Can’t respond to the next major crisis

Generational theft: Current generations benefiting at the expense of future ones

Risk of sudden crisis: Low probability, but if it happens, it would be catastrophic

The math is pretty brutal: we have a structural mismatch between what we’ve promised to spend (especially on Social Security, Medicare, and interest) and what we collect in taxes. And that gap is only growing.

Where Does the Money Actually Go?

The federal budget breaks down into three buckets:

1. MANDATORY SPENDING (~63% of the budget)

This is spending that happens automatically by law unless Congress changes the law. It’s called “mandatory” because it doesn’t require annual votes.

The Big Three:

Social Security: ~$1.5 trillion - Retirement and disability checks to elderly and disabled Americans

Medicare: ~$1 trillion - Healthcare for people 65+

Medicaid: ~$600 billion - Healthcare for low-income Americans

Other safety net: ~$500 billion (food stamps, unemployment, child tax credits, etc.)

These programs grow automatically because:

More people are retiring (Baby Boomers)

Healthcare costs keep rising

Benefits are indexed to inflation

This is the structural problem everyone’s worried about. Politicians don’t have to vote on these every year—they just keep growing. And both parties are terrified to touch them because cutting Social Security or Medicare is political suicide.

2. DISCRETIONARY SPENDING (~27% of the budget)

This is what Congress actually votes on every year in appropriations bills. It’s split into:

Defense (~$900 billion):

Military operations, equipment, personnel

Veterans benefits (~$134 billion)

Nuclear weapons programs

Military construction

Non-Defense (~$959 billion): From that chart pack, it breaks down to:

Transportation: $130B (roads, airports, trains)

Veterans Services: $134B

Education: $121B

Health Research/CDC/NIH: $100B

International Affairs: $78B

Natural Resources/Energy/Environment: $78B

Science/NASA/Tech: $41B

Everything else: Justice system, community development, agriculture, etc.

3. INTEREST ON THE DEBT (~10% and GROWING FAST)

$881 billion in 2024, and climbing rapidly

This is the part that does absolutely nothing except pay for past borrowing

Growing faster than anything else because both debt and interest rates are up

The “Just Print Money” Problem

I suggested that Trump ran his businesses by leveraging and borrowing against wealth, but has a history of defaulting on loans… whats his bankrupty count at now? 6? Anyway… he’s spending money he doesn’t have because he knows he doesn’t face consequences about anything.

Here’s where your Trump comparison gets interesting—but also where the analogy breaks down:

What Trump did with his businesses:

Borrowed heavily

When things went bad, declared bankruptcy 6 times

Walked away, creditors ate the losses

He personally never really faced consequences

What happens with a country: The U.S. can print money (we control our own currency), but there are consequences:

Inflation: If you just print to pay debts, the dollar loses value. Everyone’s savings become worth less.

Loss of trust: If investors think we’ll just inflate away the debt, they demand higher interest rates to compensate

Currency collapse: In extreme cases (think Zimbabwe, Weimar Germany), the currency becomes worthless

The U.S. has gotten away with high debt for a long time because:

The dollar is the world’s reserve currency

Treasury bonds are seen as the safest investment on earth

We’ve always paid our debts

But that’s based on trust and reputation. If that trust breaks, everything breaks.

The Current Political Reality

Recent negotiations revealed plans for a $2.5 trillion spending cut in exchange for a $1.5 trillion debt ceiling increase Wikipedia. But here’s the catch:

What CAN’T realistically be cut much:

Social Security (political third rail)

Medicare (another third rail)

Interest payments (legally required)

Defense (both parties love it for different reasons)

Those four things are roughly 80% of the budget. So when politicians talk about “cutting $2.5 trillion,” they’re either:

Not being serious

Planning to gut everything else to the bone

Planning to cut mandatory programs (political suicide)

What COULD be cut: That $959B in non-defense discretionary—but even cutting ALL of it wouldn’t close the deficit, and you’d be eliminating: veterans services, education, transportation, science research, environmental protection, justice system, etc.

The Bottom Line

Your instinct is right: there’s a bankruptcy playbook mentality at work—borrow big, don’t worry about paying it back. The difference is:

Trump’s companies: He could walk away. Creditors lose, he moves on.

The U.S. government: We can’t walk away. If we default or inflate away the debt, everyone suffers—including the people making the decisions and their families.

The real problem isn’t any one president (Biden added $8.5T, Trump added plenty in his first term, Obama added a bunch, etc.). The real problem is the structural mismatch: we’ve promised more in benefits than we’re willing to pay in taxes, and neither party wants to be the one to fix it because:

Raising taxes loses elections

Cutting benefits loses elections

So everyone kicks the can down the road

Despite talk of cost-cutting, spending actually rose $142 billion in the first half of 2025, largely due to automatic growth in Social Security and Medicare. (Committee for a Responsible Federal Budget)

The math is pretty brutal: you can’t cut your way out of this without touching the big programs, and you can’t tax your way out without massive tax increases. The only real solutions involve both—and political pain that nobody wants to inflict.

I learned a lot diving into this alongside Claude, so wanted to share it for anyone that didn’t want to go down that path.

Just because OpenAI stole all the art doesn’t mean LLMs are intrinsically bad, this is a great example of doing research when you don’t know where to look or even know what you don’t know.

Thanks for writing this, it clarifies a lot, like your other deep divez. It's cool how you leveraged AI for the initial data parsing, though those "Oh Crap" metrics on interest payments are a stark reality check.